ZeroHedge.com:

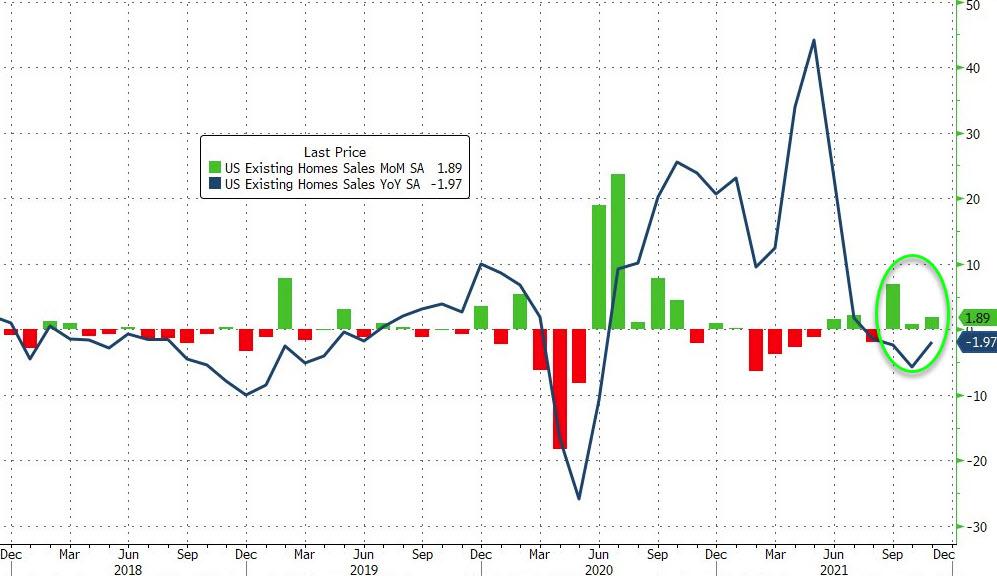

After slowing its acceleration dramatically last month, analysts expected a considerable 3.0% jump MoM in December, and while they were right in direction, the amplitude was considerably less with a mere 1.9% MoM rise.

That is third straight monthly gain and leaves existing home sales down 1.97% YoY.

Source: Bloomberg

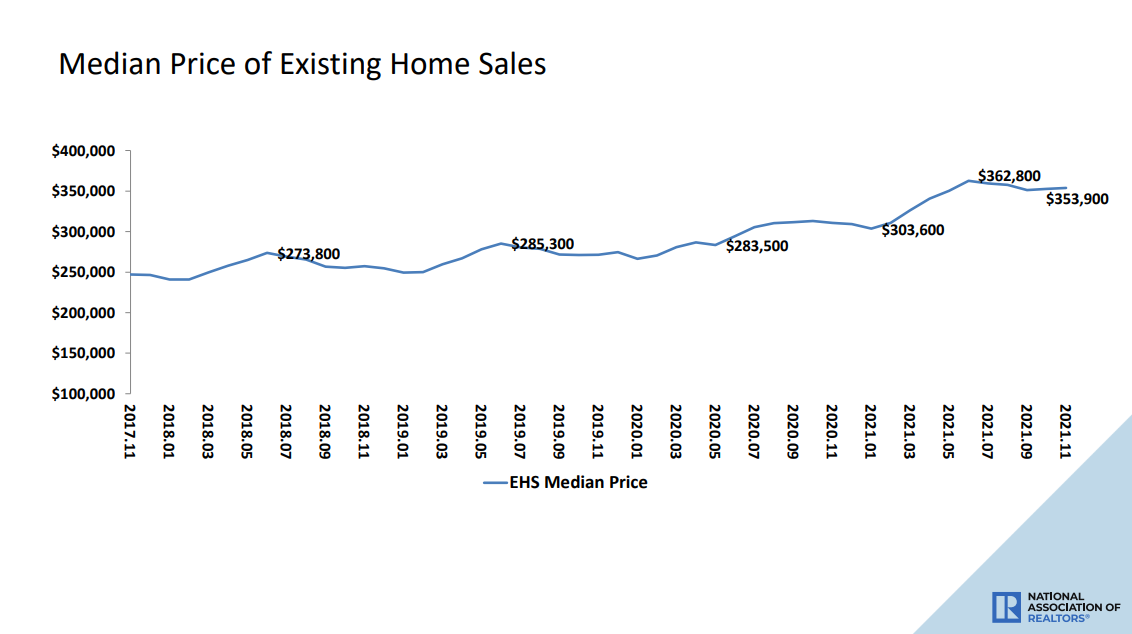

The median selling price of an existing home rose 13.9% from a year ago to $353,900 in November, reflecting in part more sales of higher-end properties, according to NAR’s data.

This marks 117 straight months of year-over-year increases, the longest-running streak on record.

Total housing inventory at the end of November amounted to 1.11 million units, down 9.8% from October and down 13.3% from one year ago (1.28 million). Unsold inventory sits at a 2.1-month supply at the current sales pace, a decline from both the prior month and from one year ago. Inventory of homes priced less than $500,000 remains tight.

“Supply-chain disruptions for building new homes and labor shortages have hindered bringing more inventory to the market,” said Yun.

“Therefore, housing prices continue to march higher due to the near record-low supply levels.”

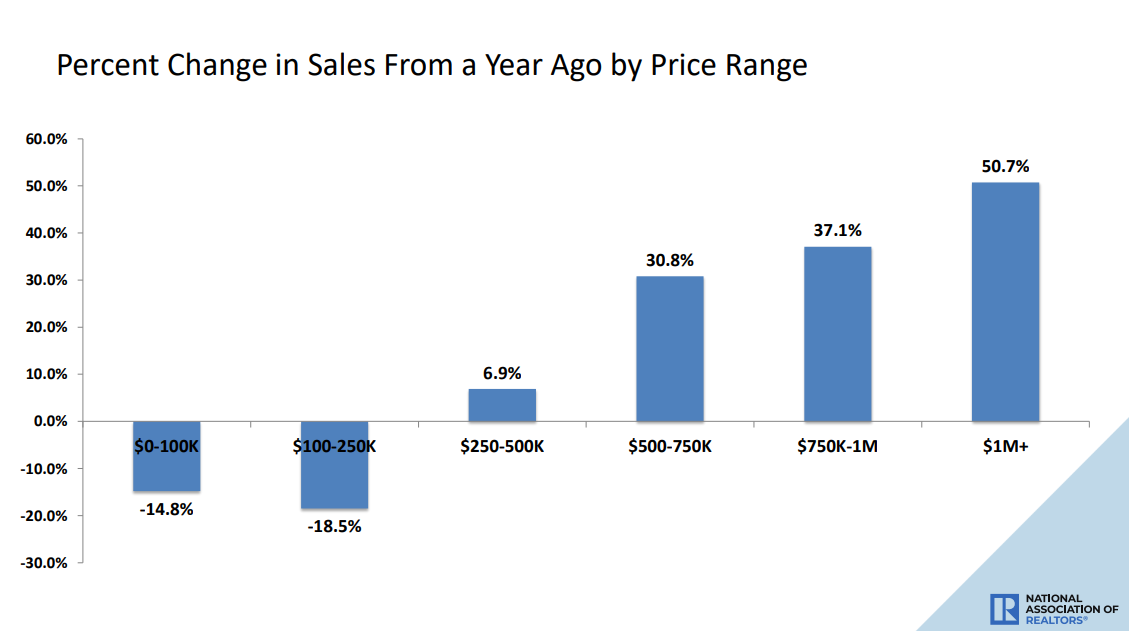

And its the most expensive homes that are seeing the biggest price rises…

Yun said sales this year are on pace to reach 6.1 million unit, which would be the best since 2006.

“Locking in a constant and firm mortgage payment motivated many consumers who grew weary of escalating rents over the last year,” he said.

Finally, first-time buyers comprised just 26% of November transactions, down from 32% a year ago and matching the lowest share since 2014 as Wall Street increases its role as America’s landlord. All-cash sales accounted for 24% of transactions in November, while investors — who make up many of the cash sales — comprised 15% of November contract signings.

“Determined buyers were able to land housing before mortgage rates rise further in the coming months,” Lawrence Yun, NAR’s chief economist, said in a statement.

NAR’s Yun admitted that “first time homebuyers are really struggling… reflecting a divided society.”

Welcome to Renter Nation America.

READ MORE at ZeroHedge.com

{kind=link}

{kind=link}

{kind=link}

{kind=link}