MarketWatch.com:

The housing market went through the wringer in 2022 as rates surged and buyers were pushed out

The housing market is nothing if not unpredictable.

Mortgage rates have skyrocketed, and the market has taken a beating. But don’t expect 2023 to turn into a buyer’s market just yet, housing experts say.

Home sales have plummeted across the board, with sales of existing homes dropping for 10 months in a row, a new record. And home-price growth has stalled.

Will 2023 will be a good year for prospective buyers? It depends on your location and your income, Odeta Kushi, deputy chief economist at First American, told MarketWatch.

Others are less optimistic. “2023 will shape up to be a nobody’s market. Neither sellers nor buyers will see any significant headway,” George Ratiu, manager of economic research at Realtor.com, told MarketWatch.

“For sellers, the reality is that the prices that they were hoping to get based on the last few years are simply no longer there,” Ratiu explained. “For buyers, prices have shot up so high in the last two years that even a 10% to 20% discount is not going to get them a bargain.”

Here’s how experts see the housing market playing out in 2023.

Good news: More homes for sale

The experts mostly agree that inventory — the number of homes available for sale — will increase in 2023.

“We will have more inventory than in the last two years,” Ratiu said. But homes for sale are staying on the market longer, he added.

Redfin Corp. RDFN, 10.39% deputy chief economist Taylor Marr said that the typical home has been sitting on the market for about two months now. “There are a lot of homes out there just waiting for a buyer,” he said.

Builders are also putting new homes on the market and are pulling out all the stops to boost sales.

In some markets out West, buyers can expect “much more inventory than before the pandemic,” Jeff Tucker, senior economist at Zillow Z, 1.58%, told MarketWatch.

Markets like Phoenix and Las Vegas, which saw a boom in sales during the pandemic, are now experiencing a glut of homes for sale.

Markets like Phoenix and Las Vegas, which saw a boom in sales during the pandemic, are now experiencing a glut of homes for sale, Tucker said. “There are a lot of homes on the market, and that does put downward pressure on prices,” he noted.

In most of the big markets, there are a couple of reasons that inventory is low.

“There is less inventory because homeowners are unwilling to give up their ultralow mortgage rates,” Lawrence Yun, chief economist and senior vice president of research at the National Realtors Association, told MarketWatch.

“Most people refinanced into an approximately 3% rate in 2020 and 2021,” he added. “Selling and [then] buying a new home means having a 6.5% mortgage rate, so even a trade-down in home size and price will mean a higher monthly mortgage payment.”

Some homeowners are turning to the rental market instead of dealing with a tough selling environment.

Good news: Less competition, goodbye to bidding wars

Many homeowners will not so fondly recall the frenzied pandemic days of intense bidding and going over budget just to close a deal on a home.

Given the sharp decline in housing sales, bidding wars may become a relic of the pandemic era in 2023.

“The buying conditions … will be unambiguously better for buyers in 2023,” Tucker said, “especially in the first half of the year, compared to the first half of 2022.”

“The buying conditions … will be unambiguously better for buyers in 2023, especially in the first half of the year, compared to the first half of 2022.” — Jeff Tucker, senior economist, Zillow

Buying conditions include the number of homes to choose from, the competition for those homes, being forced to go above list price, “and some other ancillary aspects of that, like feeling rushed because every home gets snapped up in a single weekend,” Tucker said.

Under pressure, many buyers had waived contingencies like financing, appraisals or inspections, he added. Those pressures have eased as the market has cooled down.

“Because the market has softened so much, all those buying conditions will be a lot more favorable for buyers, especially compared to the frenzied market conditions of the first half of last year,” Tucker said. “So that’s really good news for buyers.”

According to a Realtor.com survey from the fall, a growing share of sellers said that buyers are asking for repairs to be made following home inspections.

The housing market is “tilting away from the hypercompetitive environment where sellers pretty much called the shots to one in which buyers have a lot more negotiating power,” Ratiu noted.

Bad news: Mortgage rates will stabilize but won’t come down that much

Mortgage rates have soared over the last year, but buyers can expect them to stabilize and even fall slightly.

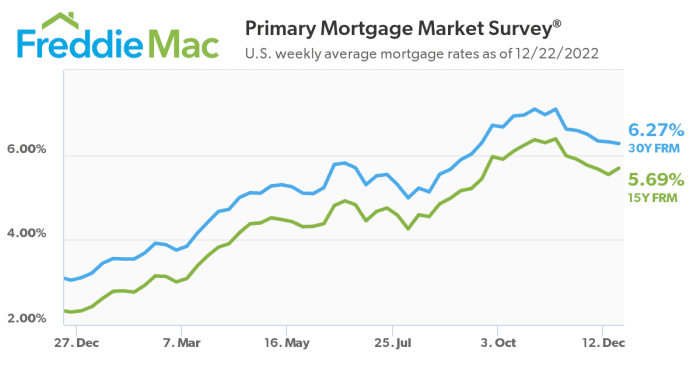

The rise in rates is the housing story of 2022, as the U.S. Federal Reserve slammed the brakes on an ultralow-rate environment, making mortgages more expensive.

Here’s how rates have surged over the past year, effectively doubling and even hitting 7% in November 2022:

“Mortgage rates are very tough to forecast. But there is reason to believe that we’ll see mortgage rates start to stabilize next year as inflation stabilizes a bit,” Kushi said, “so that will help on the … affordability and consumer-confidence front.”

Kushi said that the consensus forecast is for rates to end 2023 at around 6%.

The Mortgage Bankers Association, meanwhile, expects rates to fall to 5.4% by the end of 2023.

“We’ve seen mortgage rates surge tremendously this year, adding roughly between $800 to $1,000 a month extra to the monthly payment simply compared to a year ago,” Ratiu said.

Expect rates to remain elevated, he added, which means that if incomes don’t rise as much, then “the cost of financing a home purchase will remain expensive.”

Bad news: Home prices will drop in some markets but will still be expensive

Given the jump in interest rates, many prospective buyers are staying on the sidelines. And that’s weighing on home prices.

But don’t expect deep discounts — or a housing crash.

Mark Zandi, chief economist at Moody’s Analytics, told MarketWatch that he expects home prices in the U.S. to fall by as much as 10% peak to trough over the next two to three years. However, you have to keep in mind that those prices have also increased by 40% since the pandemic hit.

“I don’t expect U.S. house prices to crash,” Zandi added. “Of course, if the economy suffers a recession, then the house-price declines will be more significant. But even then, a crash seems like a stretch.”

Sales of existing homes have plummeted, which has begun to put pressure on home prices. According to the NAR, the median sale price of an existing home has come down from a peak of over $410,000 in June to $370,700 in November.

Ratiu noted that many sellers have resorted to price cuts to get their home sold. “Twenty percent of the homes listed on Realtor.com had price reductions in November,” he said. “So I expect that to be a part of the market in 2023, which is good news.”

‘Twenty percent of the homes listed on Realtor.com had price reductions in November. So I expect that to be a part of the market in 2023, which is good news.’ — George Ratiu, manager of economic research, Realtor.com

Redfin said its statistics were more or less the same nationally, but in some markets, price cuts have been steeper and broader, in some places affecting more than half of homes.

“Not only are buyers able to offer under asking [price] today, but they’re also able to get credits from sellers to put toward their closing costs, and also to pay points to bring their mortgage rates down,” Marr said.

So where is the slowdown is playing out? “The West is facing the strongest house-price deceleration and price declines from the peak,” Kushi said. “Specifically, Zoom ZM, 3.75% markets that saw the biggest growth over the course of the pandemic.”

So-called Zoom markets include Salt Lake City, Utah; Boise, Idaho; and other popular second-tier cities where people moved to work remotely.

But while prices may not be increasing, they’re still expensive, particularly given that incomes have not risen as much, even in the midst of high inflation.

According to an October report from the Dallas Federal Reserve, despite the strong job market, “a majority of workers are finding their wages falling even further behind inflation,” with a median decline of 8.6% in the second quarter of 2022.

Nonetheless, if mortgage rates fall to 6% and home prices also fall, “even if incomes stay flat, that means affordability will improve relative to today,” Kushi contended. “So there’s a case to be made that affordability will improve by the end of next year.”

Falling mortgage rates and home prices will make homes slightly more affordable in 2023, but not by much. And ultimately, the market isn’t going to favor either buyers or sellers.

“Higher interest rates have sucked the power out from the sellers,” Marr said, “but it’s not necessary that buyers might find it as a big win because of how interest rates are still expected to be. So it’s a bit of a tug-of-war.”

For 2023, Marr has one piece of advice for all the prospective home buyers out there.

“Keep an eye out for changes in the market, and that includes what happens with mortgage rates,” Marr said. “If they fell by half a point, that could make the difference of your monthly payment being more affordable.”

And don’t discount homes that have been on the market for longer than usual. There may be some diamonds in the rough.

READ MORE at MarketWatch.com